You are currently browsing the tag archive for the ‘digital supply chain’ tag.

Imagine you are a supplier working for several customers, such as big OEMs or smaller companies. In Dec 2020, I wrote about PLM and the Supply Chain because it was an underexposed topic in many companies. Suppliers need their own PLM and IP protection and work as efficiently as possible with their customers, often the OEMs.

Imagine you are a supplier working for several customers, such as big OEMs or smaller companies. In Dec 2020, I wrote about PLM and the Supply Chain because it was an underexposed topic in many companies. Suppliers need their own PLM and IP protection and work as efficiently as possible with their customers, often the OEMs.

Most PLM implementations always start by creating the ideal internal collaboration between functions in the enterprise. Historically starting with R&D and Engineering, next expanding to Manufacturing, Services and Marketing. Most of the time in this logical order.

In these implementations, people are not paying much attention to the total value chain, customers and suppliers. And that was one of the interesting findings at that time, supported by surveys from Gartner and McKinsey:

- Gartner: Companies reported improvements in the accuracy of product data and product development as the main benefit of their PLM implementation. They did not see so much of a reduced time to market or reduced product development costs. After analysis, Gartner believes the real issue is related to collaboration processes and supply chain practices. Here the lead times did not change, nor did the number of changes.

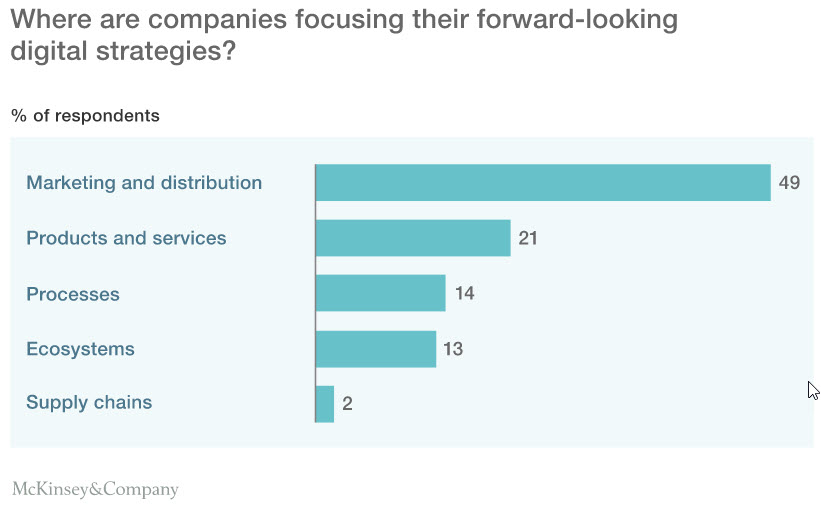

- McKinsey: In their article, The Case for Digital Reinvention, digital supply chains were mentioned as the area with the potential highest ROI; however, as the image shows below, it was the area with the lowest investment at that time.

In 2020 we were in the middle of broken supply chains and wishful thinking related to digital transformation, all due to COVID-19.

In 2020 we were in the middle of broken supply chains and wishful thinking related to digital transformation, all due to COVID-19.

Meanwhile, the further digitization in PLM (systems of engagement) and the new topic, Sustainability of the supply chain, became visible.

Therefore it is time to make a status again, also driven by discussions in the past few weeks.

The old “connected” approach (loose-loose).

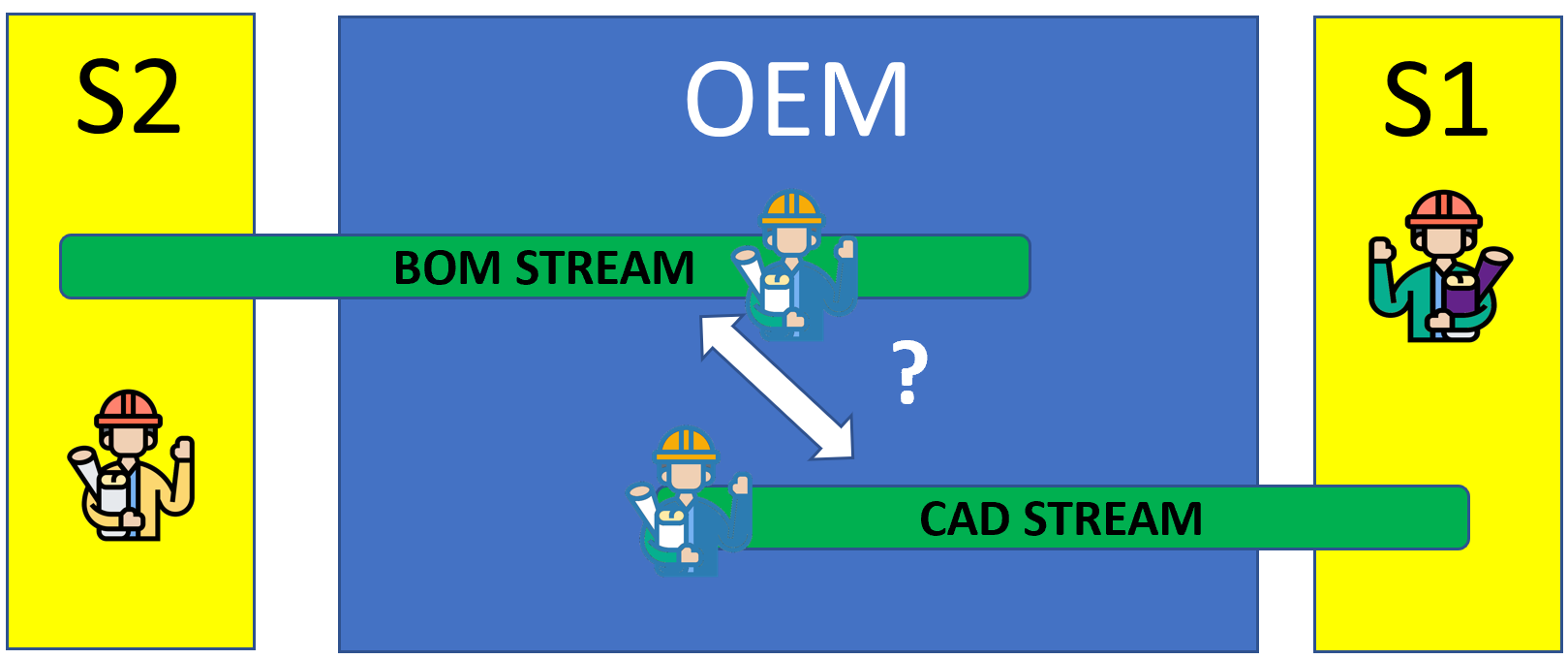

A preferred way for OEMs in the past was to have the Supplier or partner directly work in their PLM environment. The OEM could keep control of the product development process and the incremental maturity of the BOM, where the Supplier could connect their part data and designs to the OEM environment. T

A preferred way for OEMs in the past was to have the Supplier or partner directly work in their PLM environment. The OEM could keep control of the product development process and the incremental maturity of the BOM, where the Supplier could connect their part data and designs to the OEM environment. T

The advantage for the OEM is clear – direct visibility of the supplier data when available. The benefit for the Supplier could also be immediate visibility of the broader context of the part they are responsible for.

However, the disadvantages for a supplier are more significant. Working in the OEM environment exposes all your IP and hinders knowledge capitalization from the Supplier. Not a big thing for perhaps a tier 3 supplier; however, the more advanced the products from the Supplier are, the higher the need to have its own PLM environment.

However, the disadvantages for a supplier are more significant. Working in the OEM environment exposes all your IP and hinders knowledge capitalization from the Supplier. Not a big thing for perhaps a tier 3 supplier; however, the more advanced the products from the Supplier are, the higher the need to have its own PLM environment.

Therefore the old connected approach is a loose-loose relationship in particular for the Supplier and even for the OEM (having less knowledgeable suppliers)

The modern “connected” approach (wins t.b.d.)

In this situation, the target infrastructure is a digital infrastructure, where datasets are connected in real-time, providing the various stakeholders in engagement access to a filtered set of data relevant to their roles.

In this situation, the target infrastructure is a digital infrastructure, where datasets are connected in real-time, providing the various stakeholders in engagement access to a filtered set of data relevant to their roles.

In my terminology, I refer to them as Systems of Engagement, as the target is that all stakeholders work in this environment.

The counterpart of Systems of Engagement is the Systems of Record, which provides a product baseline, manufacturing baseline, and configuration baseline of information consumed by other disciplines.

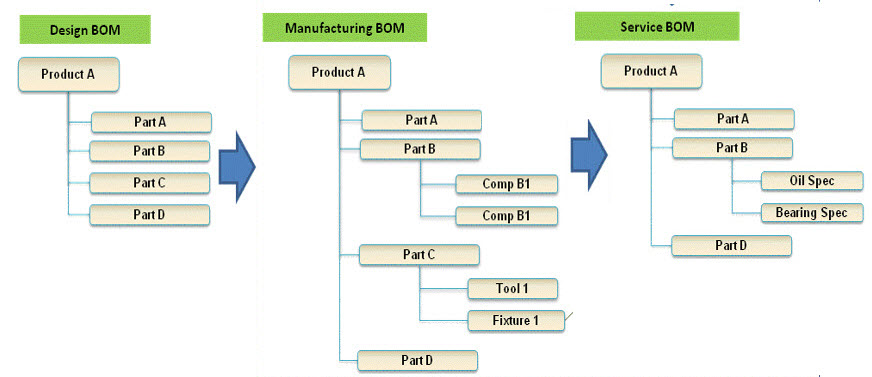

These baselines are often called Bills of Information, and the traditional PLM system has been designed as a System of Record. Major Bills of Information are the eBOM, the mBOM and sometimes people talk about the sBOM(service BOM).

These baselines are often called Bills of Information, and the traditional PLM system has been designed as a System of Record. Major Bills of Information are the eBOM, the mBOM and sometimes people talk about the sBOM(service BOM).

Typical examples of Systems of Engagement I have seen in alphabetical order are:

- Arena Solutions has a long-term experience in BOM collaboration between engineering teams, suppliers and contract manufacturers.

- CATENA-X might be a strange player in this list, as CATENA-X is more a German Automotive consortium targeting digital collaboration between stakeholders, ensuring security and IP protection.

- Colab is a provider of cloud-based collaboration software allowing design teams and suppliers to work in real time together.

- OnShape – a cloud-based collaborative product design environment for dispersed engineering teams and partners.

- OpenBOM – a SaaS solution focusing on BOM collaboration connected to various CAD systems along with design teams and their connected suppliers

These are some of the Systems of Engagement I am aware of. They focus on specific value streams that can improve the targeted time to market and product introduction efficiency. In companies with no extensive additional PLM infrastructure, they can become crucial systems of engagement.

The main challenge for these systems of engagement is how they will connect to traditional Systems or Records – the classical PLM systems that we know in the market (Aras, Dassault, PTC, Siemens).

The main challenge for these systems of engagement is how they will connect to traditional Systems or Records – the classical PLM systems that we know in the market (Aras, Dassault, PTC, Siemens).

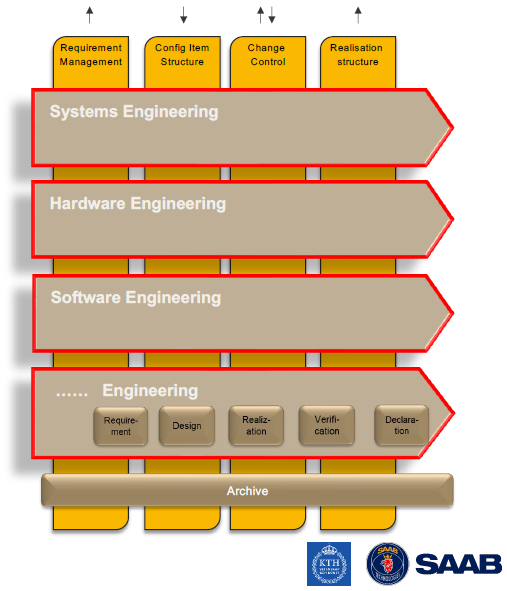

Image on the left from a presentation done by Eric Herzog from SAAB at last year’s CIMdata/PDT conference.

You can read more about this here.

When establishing a mix of Systems of Engagement and Systems of Record in your organization digitally connected, we will see overall benefits. My earlier thoughts, in general, are here: Time to split PLM?

The almost Connected approach

As I mentioned, in most companies, it is already challenging to manage their internal System of Record, which is needed for current operations and the traceability of information. In addition, most of the data stored in these systems is document-driven, not designed for real-time collaboration. So how would these companies collaborate with their suppliers?

The Model-Based Enterprise

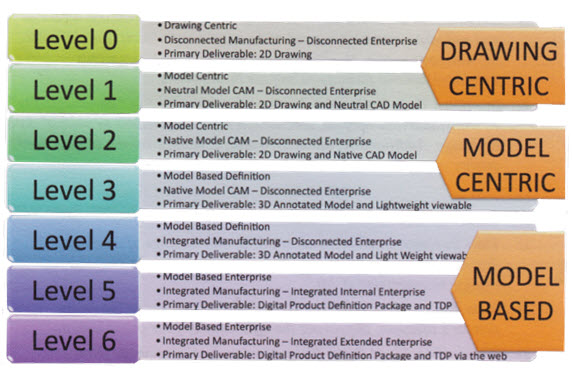

In the bigger image below, I am referring to an image published by Jennifer Herron from her book Re-use Your CAD, where she describes the various stages of interaction between engineering, manufacturing and the extended enterprise.

In the bigger image below, I am referring to an image published by Jennifer Herron from her book Re-use Your CAD, where she describes the various stages of interaction between engineering, manufacturing and the extended enterprise.

Her mission is to promote and educate organizations in moving to a Model-Based Definition and, in the long term, to a Model-Base Enterprise.

The ultimate target of information exchange in this diagram is that the OEM and the Supplier are separate entities. However, they can exchange Digital Product Definition Packages and TDPs over the web (electronically). In this exchange, we have a mix of systems of engagement and systems of record on the OEM and Supplier sides.

Depending on the type of industry, in my ecosystem of companies, many suppliers are still at level 2, dreaming or pushed to become level 3, illustrating there is a difficult job to do – learning new practices. And why would you move to the next level?

Depending on the type of industry, in my ecosystem of companies, many suppliers are still at level 2, dreaming or pushed to become level 3, illustrating there is a difficult job to do – learning new practices. And why would you move to the next level?

Every step can have significant benefits, as reported by companies that did this.

So what’s stopping your company from moving ahead? People, Processes, Skills, Work Pressure? It is one of the most common excuses: “We are too busy, no time to improve”.

A supply chain collaboration hub

On March 21, I discussed with Magnus Färneland from Eurostep their cloud-based PLM collaboration hub, ShareAspace. You can read the interview here: PLM and Supply Chain Collaboration

I believe this concept can be compelling for a connected enterprise. The OEM and the Supplier share (or connect) only the data they want to share, preferably based on the PLCS data schema (ISO 10303-239).

In a primitive approach, this can be BOM structures with related files; however, it could become a real model-based connection hub in the advanced mode. “

Now you ask yourself why this solution is not booming.

In my opinion, there are several points to consider:

- Who designs, operates and maintains the collaboration hub?

It is likely not the suppliers, and when the OEM takes ownership, they might believe there is no need for the extra hub; just use the existing PLM infrastructure. - Could a third party find a niche market for this? Eurostep has already been working on this for many years, but adopting the concept seems higher in de BIM or Asset Management domains. Here the owner/operator sees the importance of a collaboration hub.

A final remark, we are still far from a connected enterprise; concepts like Catena-X and others need to become mature to serve as a foundation – there is a lot of technology out there -now we need the skilled people and tested practices to use the right technology and tune solutions concepts.

A final remark, we are still far from a connected enterprise; concepts like Catena-X and others need to become mature to serve as a foundation – there is a lot of technology out there -now we need the skilled people and tested practices to use the right technology and tune solutions concepts.

Sustainability demands a connected enterprise.

I focused on the Supplier dilemma this time because it is one of the crucial aspects of a circular economy and sustainable product development.

I focused on the Supplier dilemma this time because it is one of the crucial aspects of a circular economy and sustainable product development.

Only by using virtual models of the To-Be products/systems can we seriously optimize them. Virtual models and Digital Twins do not run on documents; they require accurate data from anywhere connected.

You can read more details in my post earlier this year: MBSE and Sustainability or look at the PLM and Sustainability recording on our PLM Global Green Alliance YouTube channel.

Conclusion

Due to various discussions I recently had in the field, it became clear that the topic of supplier integration in a best-connected manner is one of the most important topics to address in the near future. We cannot focus longer on our company as an isolated entity – value streams implemented in a connected manner become a must.

And now I am going to enjoy Liveworx in Boston, learning, discussing and understanding more about what PTC is doing and planning in the context of digital transformation and sustainability. More about that in my next post: The week(end) after Liveworx 2023 (to come)

I am still digesting all the content of the latest PLM Roadmap / PDT Fall 2020 conference and the new reality that starts to appear due to COVID-19. There is one common theme:

I am still digesting all the content of the latest PLM Roadmap / PDT Fall 2020 conference and the new reality that starts to appear due to COVID-19. There is one common theme:

The importance of a resilient and digital supply chain.

Most PLM implementations focus on aligning disciplines internally; the supply chain’s involvement has always been the next step. Perhaps now it is time to make it the first step? Let’s analyze.

No Time to Market improvement due to disconnected supply chains?

During the virtual fireplace chat at the PLM Roadmap/PDT conference, just as a small bonus. You can read the full story here – the quote:

Marc mentioned a survey Gartner has done with companies in fast-moving industries related to the benefits of PLM. Companies reported improvements in accuracy of product data and product development. They did not see so much a reduced time to market or reduced product development costs. After analysis, Gartner believes the real issue is related to collaboration processes and supply chain practices. Here lead times did not change, nor the number of changes.

Of course, he spoke about fast-moving industries where the interaction was done in a disconnected manner. Gartner believes that the cloud would, for sure, start creating these benefits of a reduced time to market and cost of change when the supply chain is connected.

Therefore I want to point again to an old McKinsey article named The case for Digital Reinvention, published in February 2017. Here the authors looked at the various areas of investment in digital technologies and their ROI. See the image on the left for the areas investigated and the percentage of companies that invested in these areas at that time.

Therefore I want to point again to an old McKinsey article named The case for Digital Reinvention, published in February 2017. Here the authors looked at the various areas of investment in digital technologies and their ROI. See the image on the left for the areas investigated and the percentage of companies that invested in these areas at that time.

In the article, you will see the ROI analysis for these areas. For example, the marketing and distribution investments did not necessarily have a positive ROI when disconnected from other improvement areas. Digital supply chains were mentioned as the area with the potential highest ROI. However, another important message in the article for all these areas is: You need to have a complete digitization strategy. This is a point I fail to see in many companies. Often an area gets all the attention, however as it remains disconnected from the rest, the real efficiencies are not there. The McKinsey article ends with the conclusion that the digital winners at that time are the ones with bold strategies win:

we found a mismatch between today’s digital investments and the dimensions in which digitization is most significantly affecting revenue and profit growth. We also confirmed that winners invest more and more broadly and boldly than other companies do

The “connected” supply chain

Image: A&D Action Group – Global Collaboration

Of course, the traditional industries that invented PLM have invested in a kind of connected supply chain. However, is it really a connected supply chain? Aerospace and Defense companies had their supplier portals.

A supplier had to download their information or upload their designs combined with additional metadata.

These portals were completely bespoke and required on both sides “backbreaking” manual work to create, deliver, and validate the required exchange packages. The OEMs were driving the exchange process. More or less, by this custom approach, they made it difficult for suppliers to have their own PLM-environment. The downside of this approach was that the supplier had separate environments for each OEM.

In 2006 I worked with SmarTeam on the concept of the “Supply Chain Express,” an offering that allowed a supplier to have their own environment using SmarTeam as a PDM/PLM-system the Supply Chain Express package to create an intelligent import and export package. The content was all based on files and configurable metadata based on the OEM-Supplier relation.

In 2006 I worked with SmarTeam on the concept of the “Supply Chain Express,” an offering that allowed a supplier to have their own environment using SmarTeam as a PDM/PLM-system the Supply Chain Express package to create an intelligent import and export package. The content was all based on files and configurable metadata based on the OEM-Supplier relation.

Some other PLM-vendors or implementers have built similar exchange solutions to connect the world of the OEM and the supplier.

The main characteristic was that it is file-based with custom metadata, often in an XML-format or otherwise using Excel as the metadata carrier.

In my terminology of Coordinated – Connected, this would be Coordinated and “old school.”

The “better connected” supply chain

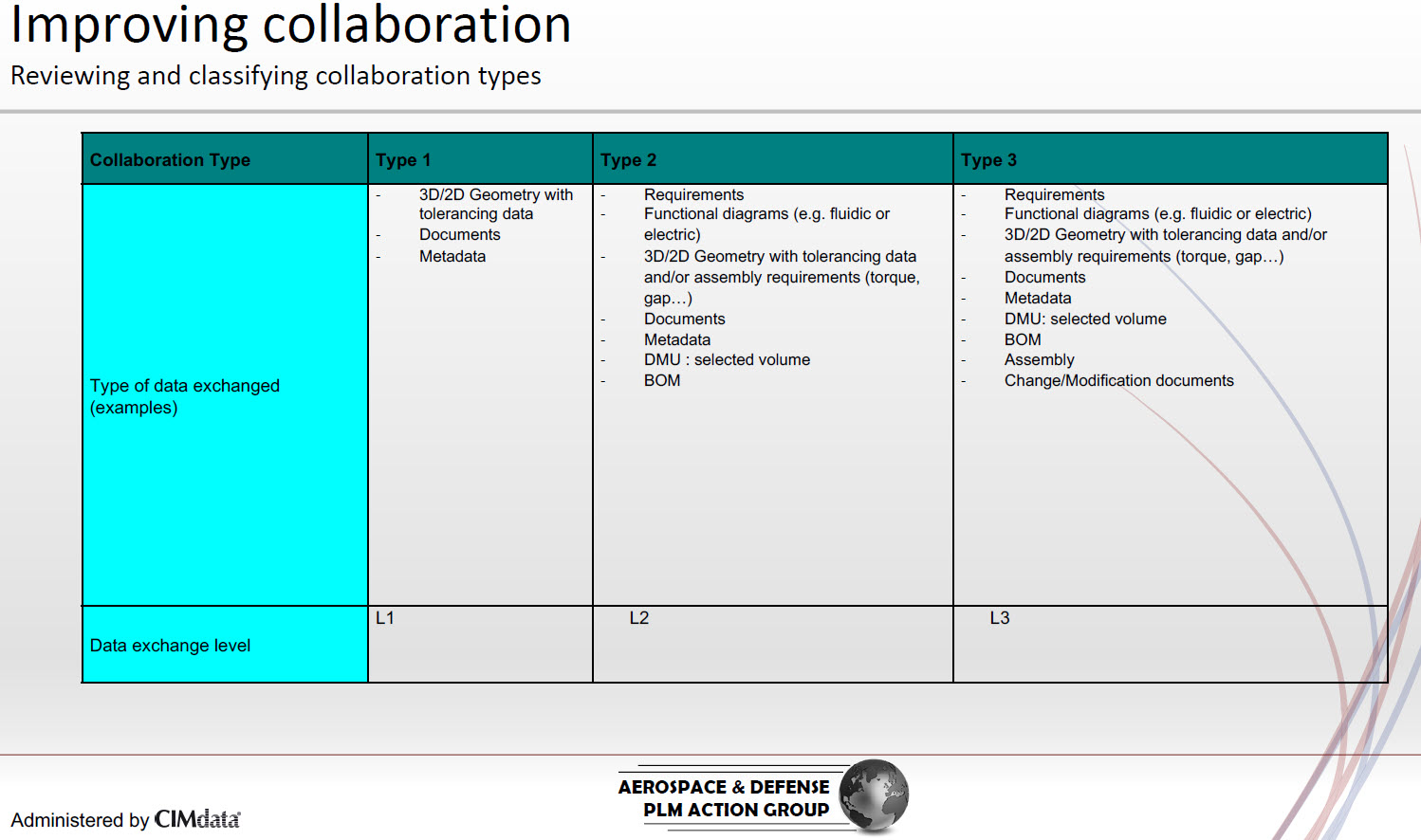

As I mentioned in my previous post about the PLM Roadmap/PDT Fall conference, Katheryn Bell (Pratt & Whitney Canada) presented the progress of the A&D Global Collaboration workgroup. As part of the activities, they classified the collaboration between the OEM and the supplier in 3 levels, as you can see from the image:

This post mainly focuses on the L1 collaboration as this is probably the most used scenario.

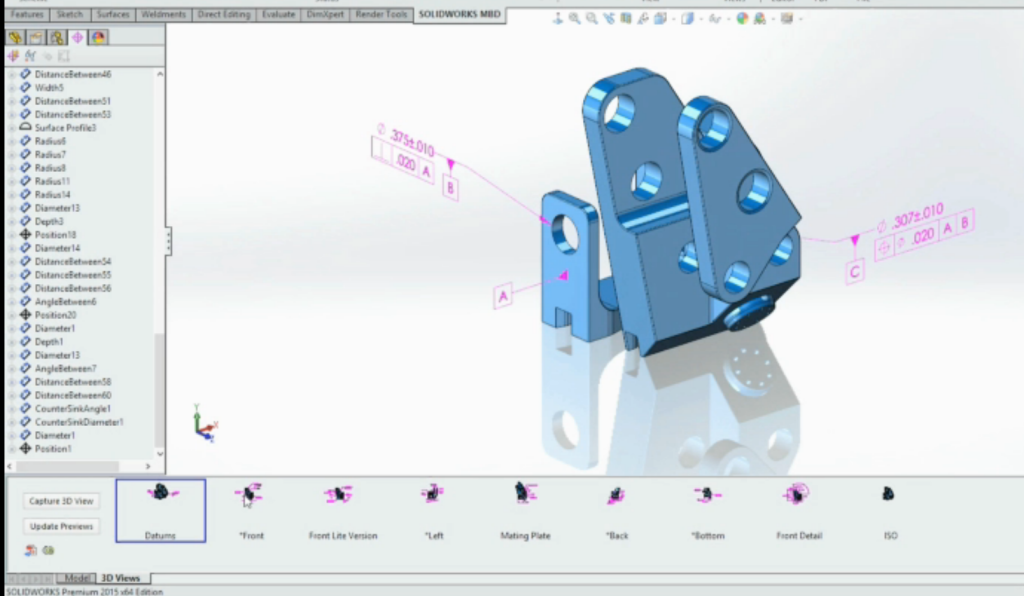

In the Aerospace and Automotive industry, the OEM and suppliers’ data exchange has improved twofold by using Technical Data Packages where the content is supported by Model-Based Definition.

In the Aerospace and Automotive industry, the OEM and suppliers’ data exchange has improved twofold by using Technical Data Packages where the content is supported by Model-Based Definition.

The first advantages of Model-Based Definition are mainly related to a consistent information package where the model is leading. The manufacturing views are explicitly defined on the 3D Model. Therefore there is a reduced chance of error for a misconnect between the “drawings” and the 3D Model.

The Model-Based definition still does not solve working with the latest (approved) version of the information. This still remains a “human-based” process in this case, and Kathryn Bell confirmed this was the biggest problem to solve.

The second advantage of using one of the interoperability standards for Model-Based Definition is the disconnect between application-specific data on the OEM side and the supplier side.

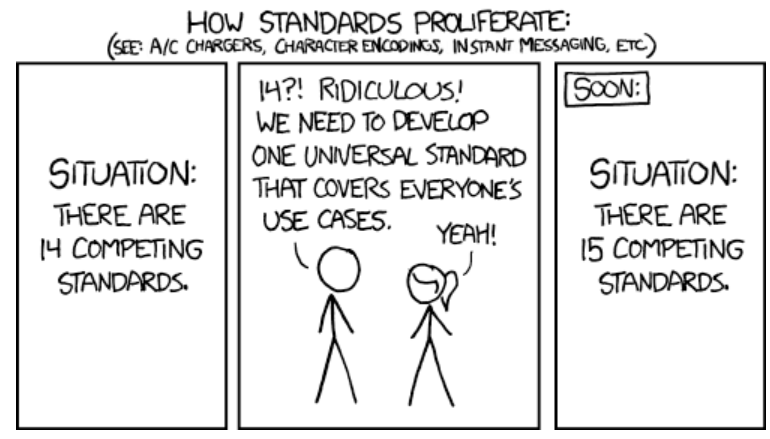

A significant advantage of Model-Based Definition is that there are a few interoperability standards, i.e., ISO 10303 – STEP, ISO14306 – JT, and ISO32000/14739 (PRC for 3D PDF). In the end, the ideal would be that these standards merge into one standard, completely vendor-independent with a clearly defined scope of its purpose.

A significant advantage of Model-Based Definition is that there are a few interoperability standards, i.e., ISO 10303 – STEP, ISO14306 – JT, and ISO32000/14739 (PRC for 3D PDF). In the end, the ideal would be that these standards merge into one standard, completely vendor-independent with a clearly defined scope of its purpose.

The benefit of these standards is also they increase the longevity of product data as the information is stored in an application-independent format. As long as the standard does not change (fast), storing data even internally in these neutral formats can save upgrade or maintenance costs.

However, I think you all know the joke below.

The connected supply chain

The ultimate goal in the long term will be the connected supply chain. Information shared between an OEM, and a supplier does not require human-based interfaces to ensure everyone works with the correct data.

The easiest way, and this is what some of the larger OEMs have done, is to consider suppliers as part of your PLM-infrastructure and give them access to all relevant data in the context of the system, the product, or the part they are responsible for. For the OEM, the challenge will be to connect suppliers – to motivate and train them to work in this environment.

The easiest way, and this is what some of the larger OEMs have done, is to consider suppliers as part of your PLM-infrastructure and give them access to all relevant data in the context of the system, the product, or the part they are responsible for. For the OEM, the challenge will be to connect suppliers – to motivate and train them to work in this environment.

For the supplier, the challenge is their IP-management. If they work for 100 percent in the OEM-environment, everything is exposed. If they want to work in their own environment, there is probably double work and a disconnect.

Of course, everything depends on the complexity of your interaction with the supplier.

With its Fusion Cloud Product Lifecycle Management (PLM), Oracle was one of the first to shift the attention to the connected supply chain.

If you search for PLM on the Oracle website, you will find it under Fusion Supply Chain and Manufacturing. It is a logical step as traditional ERP-vendors have never provided a full, rich portfolio for product design. CAD-integrations do not get a focus, and the future path to Model-Bases approaches (MBSE / MBD /MBE) is not visible at all.

If you search for PLM on the Oracle website, you will find it under Fusion Supply Chain and Manufacturing. It is a logical step as traditional ERP-vendors have never provided a full, rich portfolio for product design. CAD-integrations do not get a focus, and the future path to Model-Bases approaches (MBSE / MBD /MBE) is not visible at all.

Almost similar to what the Siemens-SAP alliance is showing. SAP more or less confirms that you should not rely on SAP PLM for more advanced PLM-scenarios but on Siemens’s offering.

For less complex but fast-moving products, for example, in the apparel industry, you see the promise of connecting all suppliers in one environment is time to market and traceability. This industry does not suffer from products with a long lifecycle with upgrades and services.

So far, the best collaboration platform in the cloud I have seen in Shareaspace from Eurostep. Its foundation based on the PLCS standard allows an OEM and Supplier to connect through their “shared space” – you can look at their supply chain offering here.

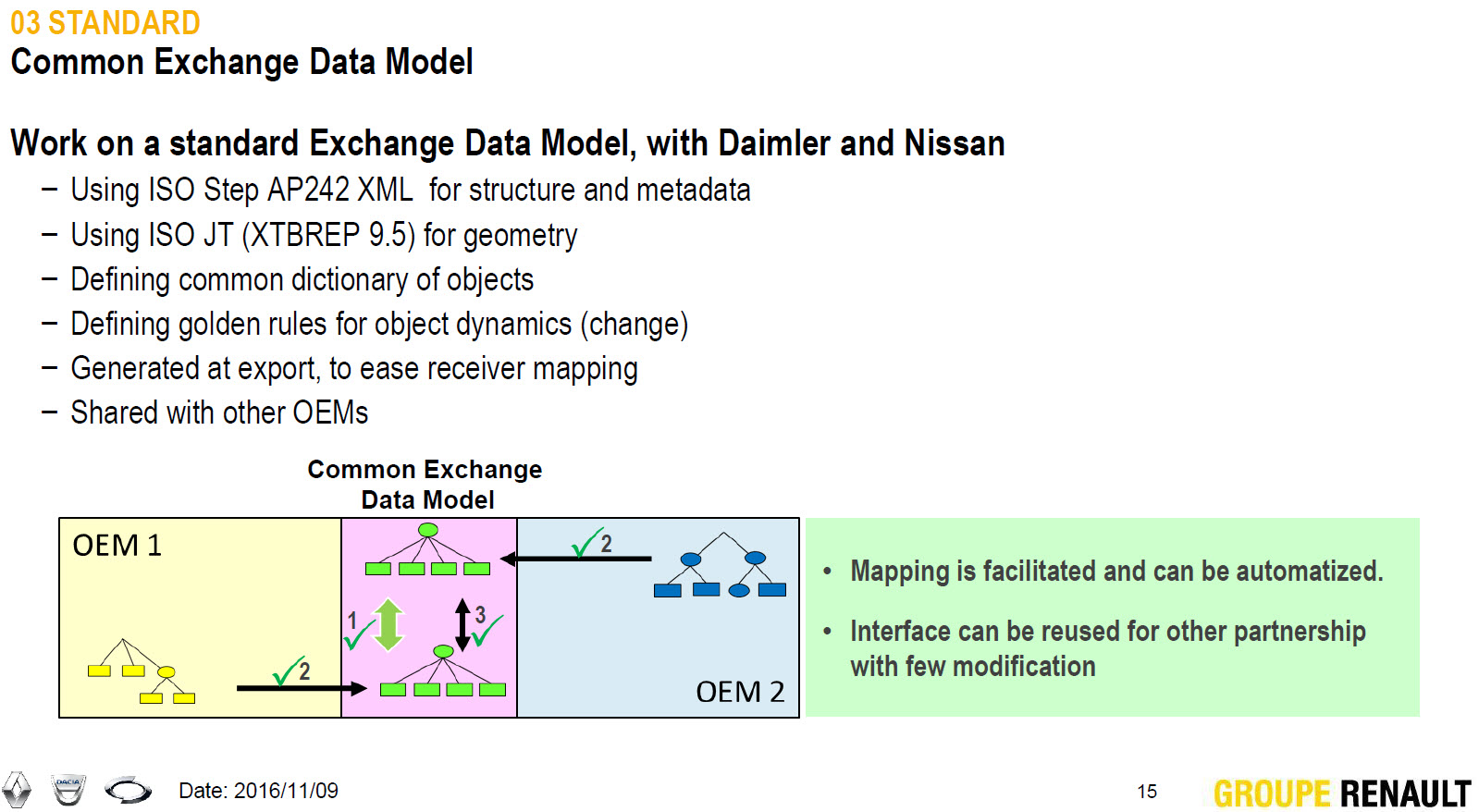

Slide: PDT Europe 2016 RENAULT PLM Challenges

In the various PDT-conferences, we have seen how even two OEMs could work in a joined environment (Renault-Nissan-Daimler) or how BAE Systems used the ShareAspace environment to collaborate and consolidate all the data coming from the various system suppliers into one standards-based environment.

In 2021, I plan to write a series of blog posts related to possible add-on services for PLM. Supplier collaboration platforms, Configuration Management, End-to-end configurators, Product Information Management, are some of the themes I am currently exploring.

Conclusion

COVID-19 has illustrated the volatility of supply chains. Changing suppliers, working with suppliers in the traditional ways, still hinder reducing time to market. However, the promise of a real connected supply chain is enormous. As Boeing demonstrated in my previous post and explained in this post, standards are needed to become future proof.

Will 2021 have more focus on the connected supply chain?

Interesting reflection, Jos. In my experience, the situation you describe is very recognizable. At the company where I work, sustainability…

[…] (The following post from PLM Green Global Alliance cofounder Jos Voskuil first appeared in his European PLM-focused blog HERE.) […]

[…] recent discussions in the PLM ecosystem, including PSC Transition Technologies (EcoPLM), CIMPA PLM services (LCA), and the Design for…

Jos, all interesting and relevant. There are additional elements to be mentioned and Ontologies seem to be one of the…

Jos, as usual, you've provided a buffet of "food for thought". Where do you see AI being trained by a…